Social Security & Retirement Financial Modeling

App details

About Social Security & Retirement Financial Modeling

Thinking about retiring? If so, Social Security & Retirement Financial Modeling, or SS&R for short, is the assistant you’ve been looking for -

SS&R:

• Is downloaded from a trusted source (Windows App Store)

• Has an unbelievably low price (about that of a cup of coffee or a gallon of gas, not the $100+ charged by others for SS&R’s capabilities)

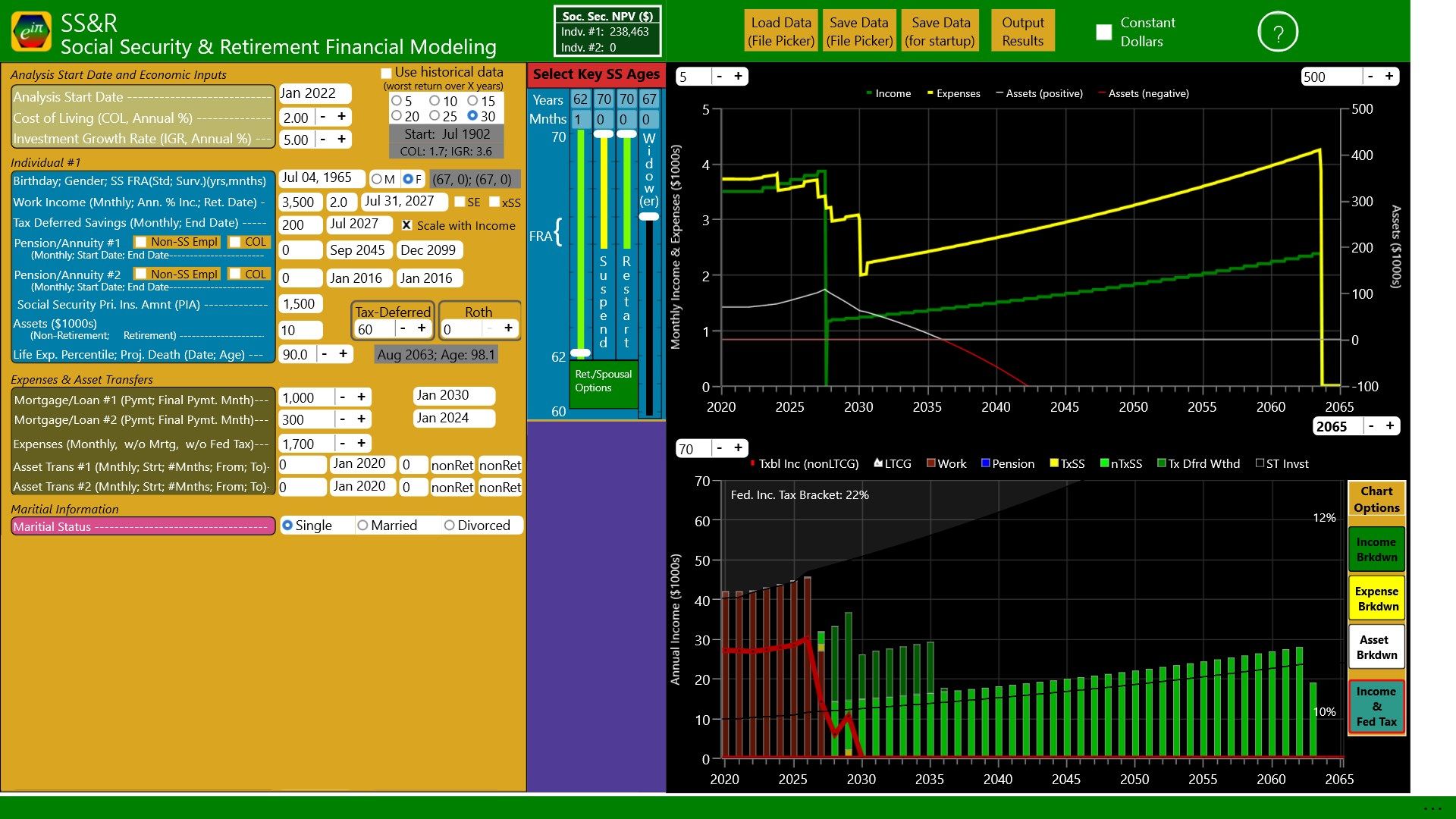

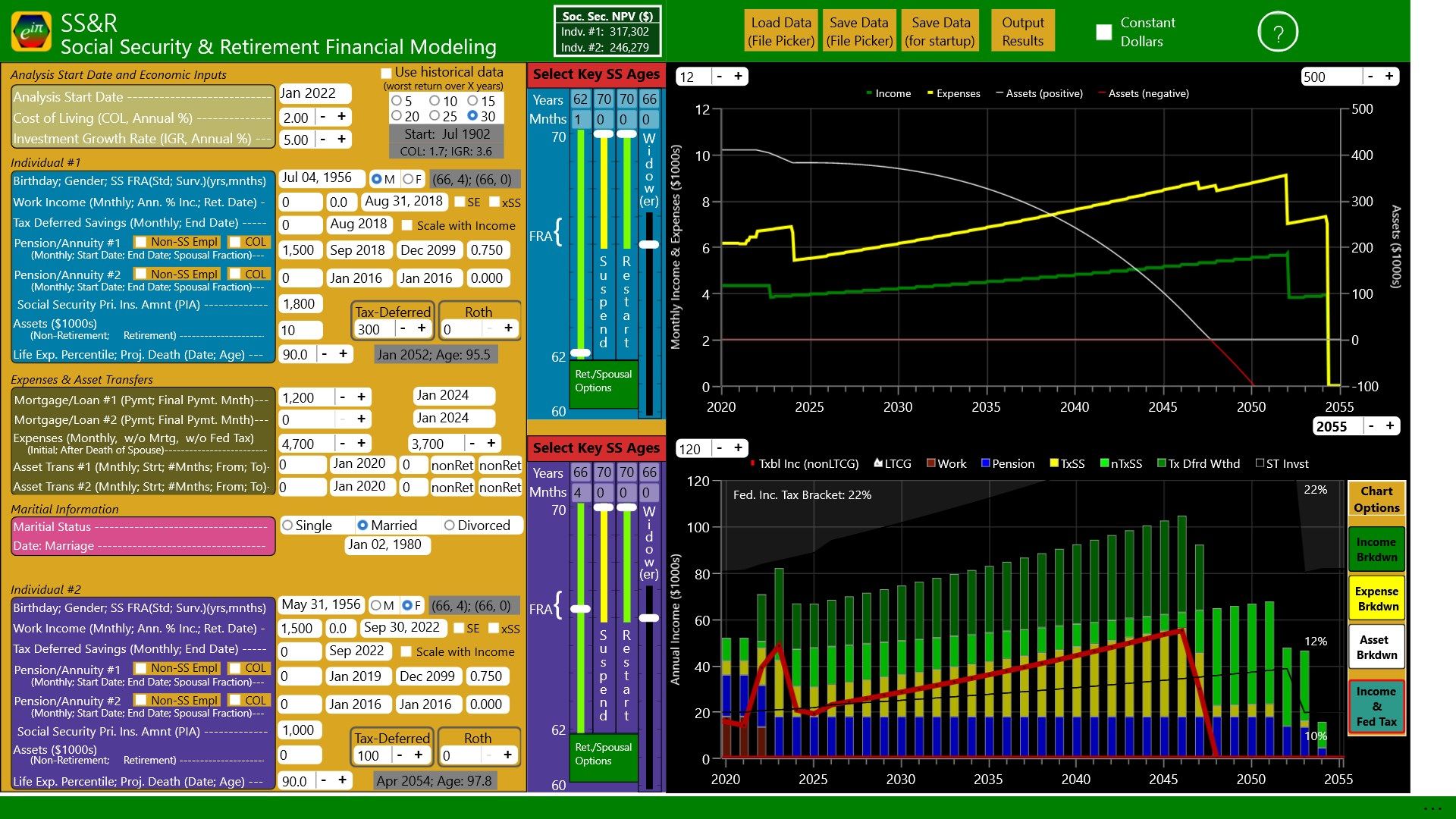

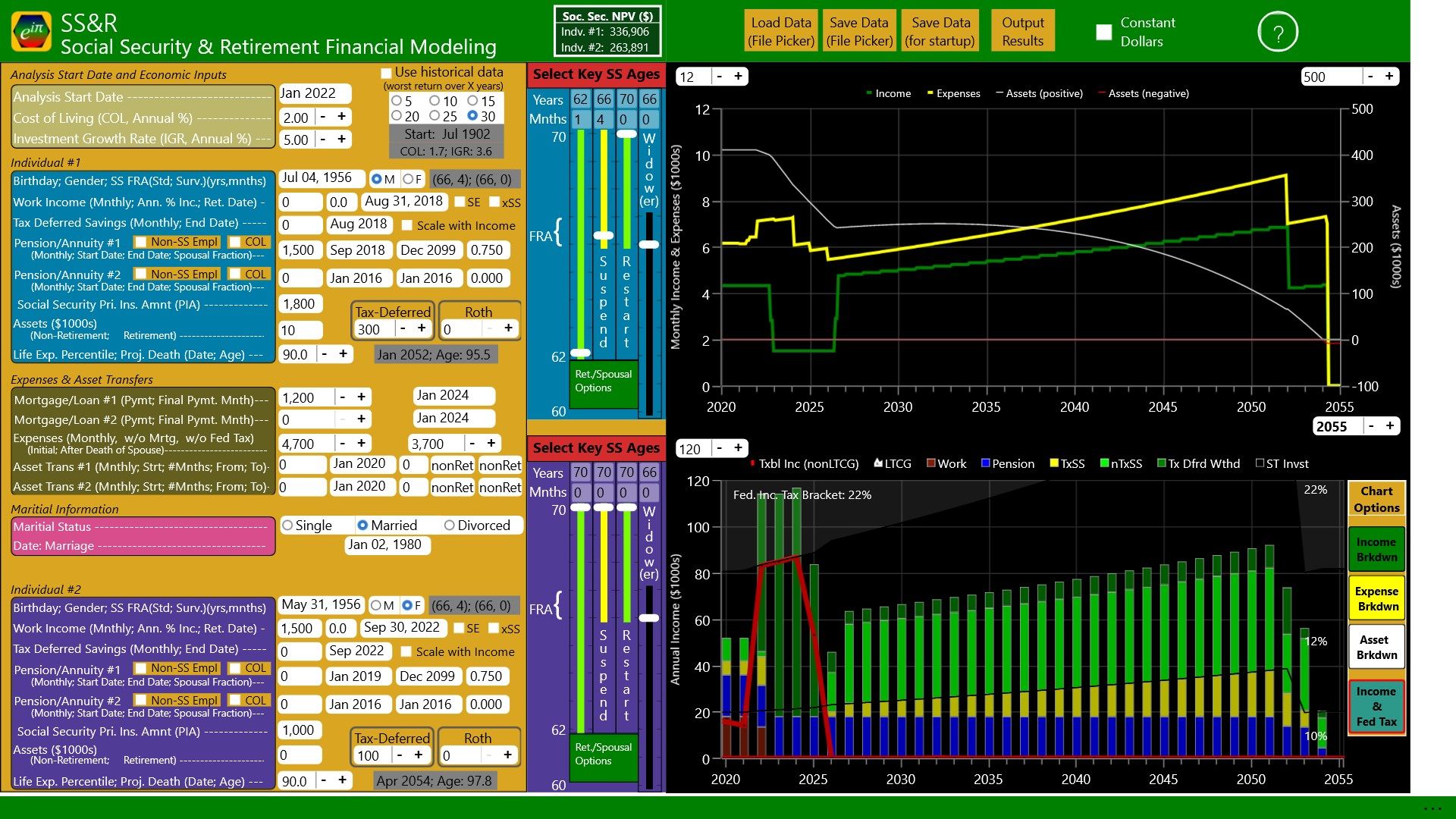

• Presents inputs and results all on a single page (see screen shots)

• Works on your computer (no data shared with anyone)

Why such a low price? eiPie Innovations is banking on volume. Approximately 10,000 people, per day, are turning 62 in the United States. The hope is that SS&R, being simple to use and providing great value, will generate good reviews and word-of-mouth testimonials. That, in turn, should drive enough sales to make the creation and ongoing development of SS&R worthwhile. (So please, provide those reviews!)

That was the sales pitch. Now a little more information about the program -

Answers to retirement questions - When can I retire? When should I start collecting Social Security? How much can I afford to spend when I’m no longer working? - are always dependent on the particulars of our situation. Primary among those particulars are: Work status, anticipated longevity, marriage situation, retirement and non-retirement savings, expenses, pensions, and potential Social Security benefits.

Given the difficulty of comprehending the interactions between income, savings, taxes, and Social Security benefits in even the short term, and given that retirement decisions can have a financial impact two, three, or even four decades down the road, help is needed to peer into the foggy future. A means to combine the particulars, handle the interactions, and project the consequences of retirement decisions into and through our retirement years would provide valuable assistance in answering our retirement questions and helping us make informed decisions.

Social Security & Retirement Financial Modeling, or SS&R for short, utilizes the pertinent particulars of a person’s, or couple’s, financial situation and projects that situation into his/her/their retirement years. The necessary information includes:

• Birthday(s)

• Marital status

• Income (monthly)

o Work (wage or self-employment)

o Pensions/annuities

• Expenses

o Mortgage

o Other expenses (excluding mortgage and federal taxes)

• Assets

o Non-retirement

o Retirement

- Tax-deferred (e.g., traditional IRA or 401K)

- Roth

o Social Security Primary Insurance Amount

Along with entering the above information, the user may specify the values used by SS&R for Cost-Of-Living and Investment Growth Rate. SS&R, utilizing the key rules of both Social Security and the IRS, then does its work to create estimates of your financial future.

What elements of Social Security and the IRS does SS&R incorporate?

For Social Security:

o Worker, spouse, and widow(er) benefits

o Impact of work on benefits

o Impact of age at which benefits are begun

o File, suspend, and restart options

o Spousal Benefit Only option (after full retirement age, and must have turned 62 on or before 1/1/2016)

o Windfall Elimination Provision (WEP)

o Government Pension Offset (GPO)

For the IRS:

o Single/married

o Wage/self-employment income

o Taxable portion of Social Security benefits

o Required Minimum Distributions (RMD) from tax-deferred retirement accounts

o Capital gains

o Alternative Minimum Tax (AMT) calculations

o FICA (i.e., Social Security) and Medicare taxes

What limitations and assumptions exist in SS&R relative to Social Security and the IRS? SS&R does not deal with Social Security benefits for children or the disabled, and does not accommodate the Social Security ‘Windexing’ provisions that may be beneficial to widows/widowers whose spouses died prior to age 62.

Relative to the IRS, calculations comprehend single or married status, but not head of household. Standard deductions are assumed, including, when appropriate, the additional deduction available to those over 65. It follows that itemized deductions are not accommodated. Since SS&R is making estimates out into future years, it is assumed the structure of federal taxes remains fixed, but tax brackets are indexed to the projected cost-of-living changes. Required Minimum Distributions from tax-deferred retirement accounts are calculated, in all cases, using the IRS’s “Uniform Lifetime Table.” (If the account owner’s spouse is more than 10 years younger than the account owner, the less demanding “Joint Life and Last Survivor Expectancy Table” would normally be used.)

It should also be mentioned that capital gains on non-retirement assets are assumed to be realized each and every year. As required by the IRS, capital losses in excess of $3000 are carried over to the following year. SS&R, with default settings, assumes gains in non-retirement assets are split evenly between long-term capital gains and ordinary income items (e.g., short-term capital gains, CD interest, and non-qualified dividends). The user, however, has the option to specify a different ratio if their non-retirement account investments are better represented by something other than a 50:50 split.

Because SS&R includes all the taxes typically encountered by Joe Taxpayer, but conservatively assumes standard deductions, tax estimates should tend to miss on the high side. Consequently, the calculation of total assets over time should tend to miss on the low side for those who benefit by itemizing deductions.

Disclaimer

SS&R, utilizing 2022 Social Security and US federal tax parameters, 2020 Social Security actuarial data (for life expectancy), inputs/assumptions concerning future market performance and cost-of-living changes, along with inputs that describe a person’s or couple’s current financial situation, strives to project that situation out into the future. The world, however, is not orderly. Paraphrasing a bumper sticker, ‘Stuff happens.’ Rules change, situations change, and it’s even possible, truth-be-told, that coding errors exist that impact the outputs of SS&R. Thus, SS&R is, and should be viewed as, a well-intentioned assistant, not a source of “Gospel truth.”

Key features

-

Project personal financial situation out through your retirement years.

-

Social Security benefits calculated based on your and/or your spouse's Primary Insurance Amounts (obtainable from Social Security) and your filing choices.

-

Accounts for impact of income from work while collecting Social Security.

-

Optimization capability to find potentially advantageous years for conversions from tax-deferred to Roth accounts.

-

Handles Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) situations

-

Ability to specify value of both non-retirement and retirement (tax-deferred and Roth) assets.

-

Handles Required Minimum Distributions from tax-deferred retirement accounts.

-

Increases miscellaneous monthly expenses (i.e., everything other than mortgage/loan payments and federal taxes) based on cost-of-living changes.

-

Accommodates single, married, and divorced situations.

-

Federal tax calculations comprehend: taxable portion of Social Security, cost-of-living impact on tax brackets , additional standard deduction for those over age 65, AMT considerations.

-

Life expectancy based on specified life expectancy percentile and actuarial tables from Social Security.

-

Ability to directly compare total assets over time for two different retirement scenarios (e.g., collecting Social Security at age 62 vs. a later starting age).

-

Ability to inject some realism into the financial projections by utilizing historical data (six different bad economic periods in US since 1871) for cost-of-living and investment returns.

-

Ability to output a tab-delimited text file of results.